Based on the FCRA’s provisions, you can recover and dispute any negative information on your report

Federal bankruptcy courts made this provision to offset debts from people and businesses. While it may help you avoid debt, you have to understand the long term consequences. Bankruptcies offer you a short-term loan relief, but its consequences can go up to a decade. Besides, a bankruptcy could cripple your negotiating capability for favorable rates of interest or credit cards. In the class of filing a bankruptcy, Credit Card Tips you are going to need to go through several legal hoops and challenges. Before filing, you are going to need to prove that you can not pay the loan and go through counseling too. Then, the thing would force you to choose between chapter 7 or chapter 13 bankruptcy. Whichever the case, you’ll pay the related fees — both court fees and attorney fees. Since you’ll likely lose home or provide up possessions for sale, avoiding it’s an perfect choice. Filing bankruptcy affects the outlook by which creditors see you, hence you ought to avoid it.

Around the united states, a credit card continues to be among the most coveted financial instruments. Undeniably, almost everyone in the US functions to have financial freedom by means of a charge card. Of course, a credit card has a wide selection of perks and lots of drawbacks too. First off, card issuers consider several elements of your own credit report before approving your application. In other words, obtaining a very low credit score would practically guarantee a flopped program. Besides, you are going to want to watch a couple of items once you get your card. Habits like defaulting, surpassing the charge utilization limit would affect your credit report and score. In addition, the application adds a hard inquiry to your report, which also affects your score. The more your application flops, the more inquiries are added to your report. In regards to utilizing the card, several exemptions adhere to high frequency standards. Failure to obey the regulations would tank your credit rating and harm your report.

Around the united states, a credit card continues to be among the most coveted financial instruments. Undeniably, almost everyone in the US functions to have financial freedom by means of a charge card. Of course, a credit card has a wide selection of perks and lots of drawbacks too. First off, card issuers consider several elements of your own credit report before approving your application. In other words, obtaining a very low credit score would practically guarantee a flopped program. Besides, you are going to want to watch a couple of items once you get your card. Habits like defaulting, surpassing the charge utilization limit would affect your credit report and score. In addition, the application adds a hard inquiry to your report, which also affects your score. The more your application flops, the more inquiries are added to your report. In regards to utilizing the card, several exemptions adhere to high frequency standards. Failure to obey the regulations would tank your credit rating and harm your report.

Defaulting can hurt your credit report and drop your credit rating significantly. Since on-time payments are among those critical boosters of your credit rating, defaulting can bite you. Your credit score could continually plummet if you already have a significantly low score. In some instances, it’s reasonable to default due to some financial crisis or unprecedented situations. In the event that you experienced any issue, your loan issuer could understand and provide you some grace period. But, making late payments as a habit could influence your muscle. The national law states that overdue payments could only be reported when they are 30 times late. Exceeding this window would affect your ability to borrow money or loans deal favorable interest prices. Continuous delinquencies would make creditors perceive you as a speculative debtor. In brief, maintaining great financial habits and making timely payments will work to your leverage.

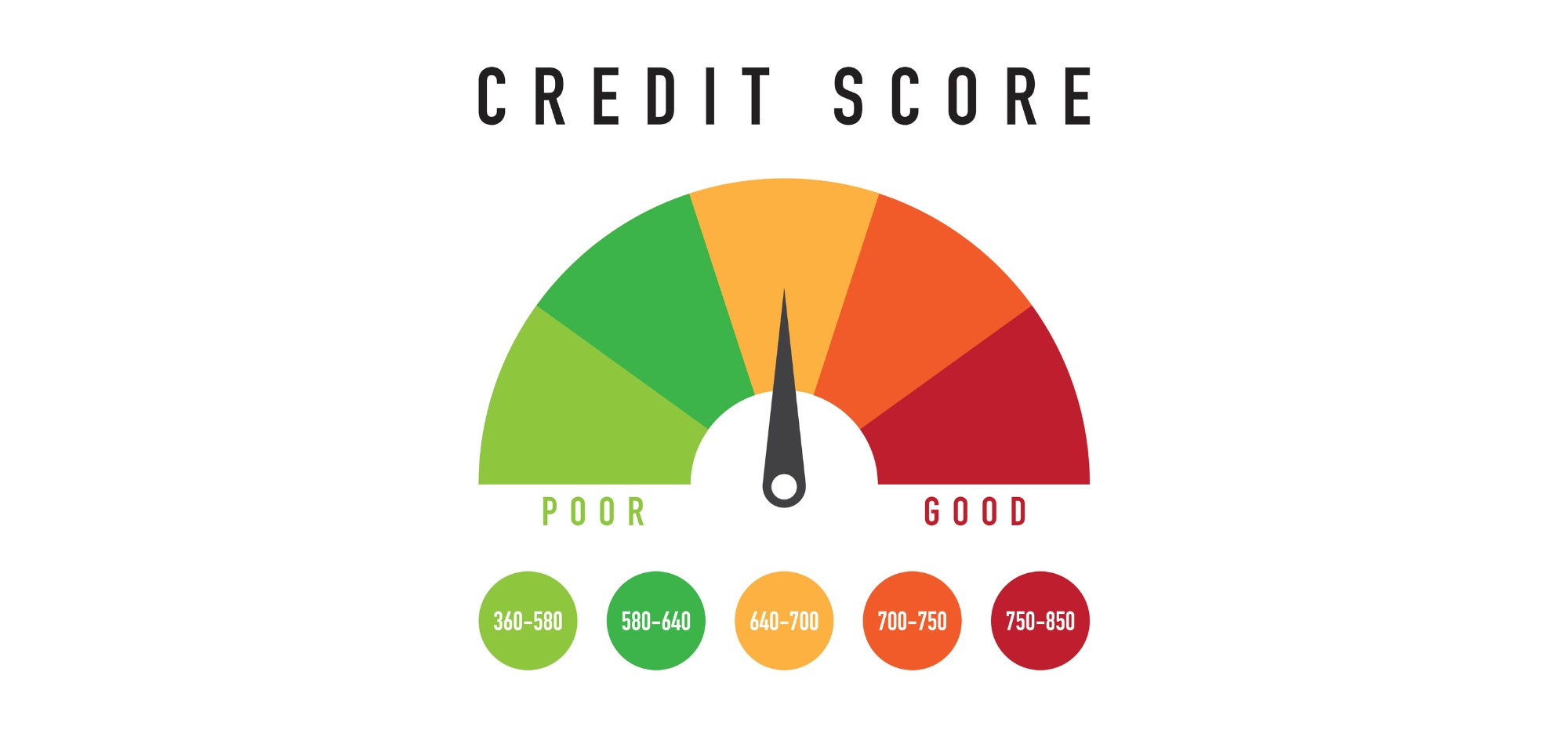

As there are plenty of items that could damage your own credit, you could be wondering if it’s the loan does. At a glance, loans and how you manage them determine the score which you’ll ever have. Since credit calculation models are generally complicated, loans can either boost or tank your credit score. Having several delinquencies would always plummet your credit rating. Should you beloved this short article in addition to you want to acquire more information relating to chototmuaban.Net generously pay a visit to our own web site. When issuing loans, lenders use your credit score to determine the type of customer you are. Because you require a loan to build an extensive history, this component may be counterintuitive. In other words, if you have not had a loan previously, your success rate could be incredibly minimal. That said, the association between loans is a linear chain, and you are going to need a loan to prove yourself. If you have had a good payment history in the past, the loan issuer might consider your program. On the contrary, your program would flop when you’ve got a history of defaulting. If you have damaged your report previously, taking a new loan might help you reestablish it. Because debt quantity accounts for a considerable portion of your report, you need to give it immense attention.

Charge Saint can be a perfect option if you choose to involve a credit repair firm. As it has got an A+ rating based on BBB, Credit Saint has lots of suitable items to offer. This company has been operating for approximately 15 decades and one of the top-ranked within this landscape. One of the greatest advantages of Credit Saint is the way that it educates consumers about various credit problems. Moreover, it has three packages– Polish, Clean Slate, and Credit Remodel — where you select. As you move about the process, the legal staff would prepare dispute letters to fit your specific requirements. One notable perk of this provider is the 90-day money-back guarantee in the event you’re not entirely satisfied. However, like any other service provider, Credit Saint has its associated downsides. The company is not available in most of the countries and has incredibly large setup fees. If you are residing in South Carolina, then you might need to look for the assistance of other service providers.

0 comentário